Many private consumers have long since taken out their insurance policies via the well-known online comparison portals such as Check24 and Verivox. Now the relevance of such online marketplaces is also becoming increasingly important for commercial insurance policies. Small businesses in particular are already taking advantage of the opportunities.

Short & Concise

- Online comparison portals are the winners in the private customer segment

- Good example for less complex risks, also for brokers

- Chance for real platforms in agile environments

Review: More than ten years ago, hardly anyone could have imagined that an online platform could dominate the market of private insurances as much as Check24, for example, has succeeded in doing. In the meantime, the service seems to increasingly determine the rules: Those who do not participate have a hard time in new customer business. The insurance industry regrets again and again on the part of the insurers, but also on the part of the brokers and consultants, that they have not taken up the issue themselves.

Whether companies use online portals for their commercial insurance policies depends on the size of the company and the respective line of business. It is also important whether the respective company risk can be represented at all in the standardised queries of online portals.

Standardised questionnaires vs. individual risk scenarios

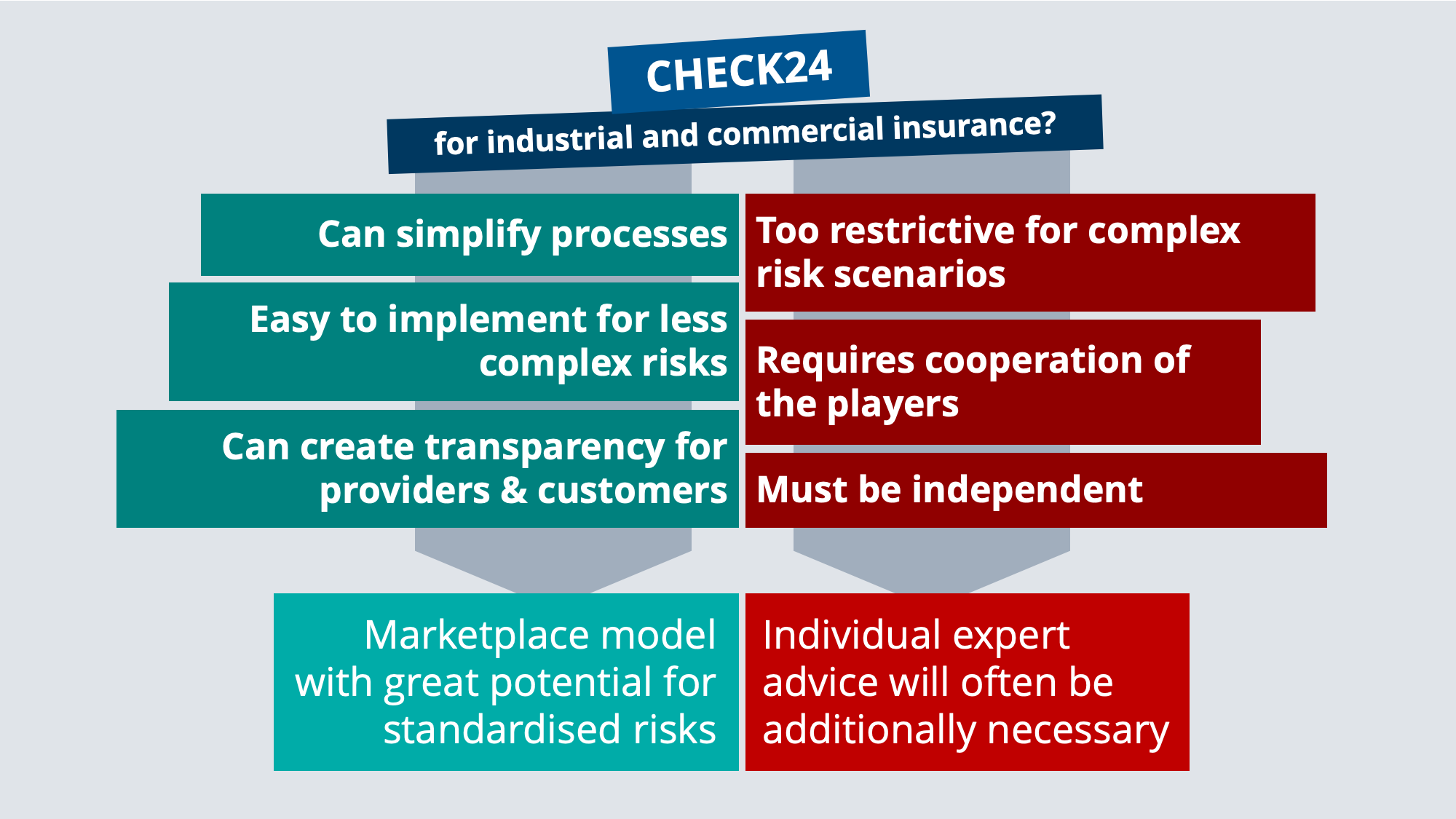

For less complex risks, online portals are a good option. However, they usually only deal with the individual risk situation of the customer to a limited extent and only process risks up to a certain depth and complexity. The necessary high degree of standardisation of the digitalised risk questionnaires sets the limits. In order to make the offer interesting for larger companies, it is therefore necessary to move away from standardised risk questionnaires, which are often far too small. This is where a broker with his experience and responsibility is needed to combine risk management and insurance management, to get a realistic picture of the overall risk situation and to offer insurance cover that actually meets the requirements.

Some online platforms from the commercial and industrial sector have responded to this need and, in addition to addressing end customers, have also been approaching brokerage houses over the last two years. In this constellation, the broker, who as an expert assesses the products and controls the closing process, becomes the customer of the online portal. In some cases, this works well – in others, even the broker who wants to insure his customers individually and to the best of his knowledge and belief reaches its limits with platform solutions. The reason is that marketplace solutions in most cases only depict standardised insurer solutions and only rarely individual protection concepts. The implementation of broker products and individual concepts is often still too costly at the moment.

A marketplace must be independent and transparent

A marketplace must be independent and transparent

A marketplace must be independent and transparent

A marketplace must be independent and transparentThe conditions, which product is listed at a certain position in the ranking of search hits, are mostly unclear in comparison portals. The often intransparent presentation of products is a difficulty for all players: for customers, for brokers, but also for insurers who are unsure how they could influence the listing of their product. Customers must be aware that portal recommendations for a particular product offered as “the best” are not automatically best suited to their personal risk situation.

Why is the industry struggling to set up such collaboration platforms?

Especially for large organisations, Inex24, a portal for industrial insurance, was launched almost ten years ago. The ambitious project had many insurers on board and set itself the goal of mapping the entire value-added chain, from risk managers to intermediaries, brokers, primary insurers and reinsurers to placement on the capital market. In the case of Inex24 the model did not work: The portal still exists, but it is not one of the relevant players.

In order for such a portal to be successful, it must be based on independence and trustworthiness from the very beginning. It is therefore essential that a critical mass of brokers and insurers participate. Moreover, the participants in such a platform must remain open to how the cooperation develops. Now that a great many companies value agile work, such a project might have better chances than ten years ago.

Conclusion

The success of Check24 & Co. is not easily transferable to the commercial and industrial customer sector. Small businesses may be well served by such a platform – but for more complex situations the expert’s eye is needed. Brokers can use platforms for commercial insurance as one tool among several. However, this does not cover all scenarios. If an online marketplace is to be successfully relaunched, independence, trustworthiness and transparency must be ensured in all cases.

This article was created in the context of a partnership of mgm and the insurance broker Gossler, Gobert & Wolters Gruppe (GGW) from Hamburg. In the series different participants write from and about the practice.

Photo: Delphotostock / Adobe Stock

Neueste Kommentare