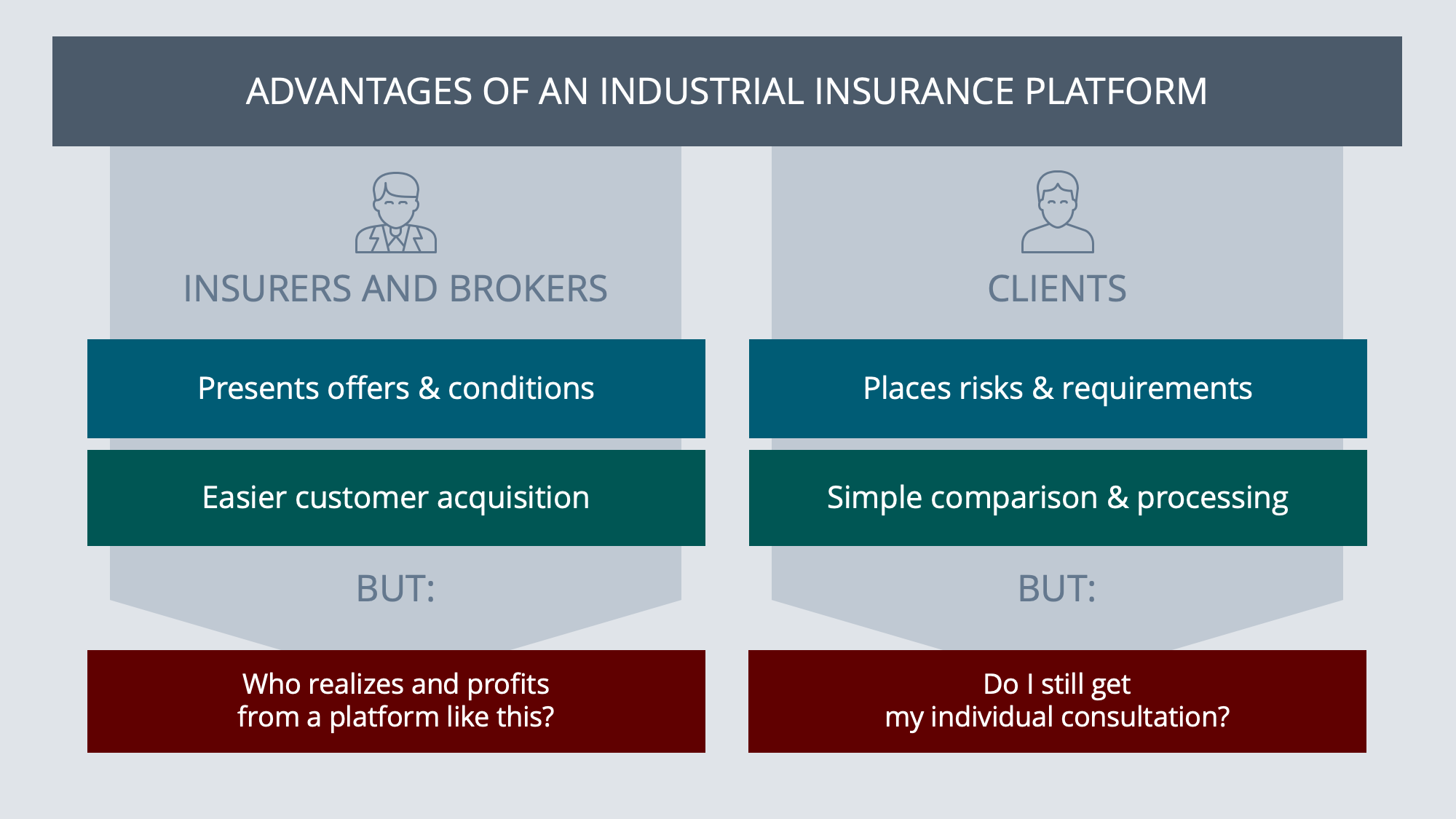

Amazon is everywhere, sometimes as a role model, sometimes as a spectre – or both at the same time. The eCommerce giant also regularly serves as a basis for discussion in the industrial insurance industry as to whether a similar solution is not possible for the industry, through which insurers and brokers can present offers and policyholders as customers can place risks.

Short & concise

- Network concept of the Internet economy & eCommerce continues to be a model for industrial insurance.

- Challenge: The mostly highly complex and individual risk structure must be reproducible.

- It is essential to counter the Internet giants at an early stage with value-added services.

An industrial insurance like Amazon would be no less than the answer to the great challenge of digitalization. However, enquiries, offers, underwriting and finally the issuing and maintenance of insurance policies for the industry are a highly complex and often ever new, individual process. After all, there are already approaches of comparison and closing portals for small businesses and freelance professions based on the model of Check24. But whether the insurance needs of medium-sized businesses and industry and true digital collaboration merely require more interfaces between the existing systems or whether the industry should join forces and jointly host a new, large-scale solution – that is the key question for the industry in the new decade.

Amazon has understood from the beginning: The more market participants participate and the larger the product offering, the greater the attractiveness and added value of the entire platform for the customer. Even though many merchants moan about Amazon’s high fees, they all follow this basic principle. The network effect is the benefit for all.

Challenge: the digital representation of the individual risk situation

“The business of offering and issuing policies, such as in the private or small business sector, is not so easy for the industry to implement,” says Benjamin Zühr, Head of Digital Solutions at the medium-sized brokerage group Gossler, Gobert & Wolters Group (GGW). “The underlying risks are simply more individual and complex. In industrial insurance, we need to give much more thought to how we can map this situation digitally”. He sees an opportunity in the close integration of insurance and risk management. Industrial customers have to provide data initially and regularly after completion: from turnover and employee numbers to locations, warehouse conditions and many other details. “If they digitally structure and measure their risks and transfer all data directly to a secure platform with brokers and insurers that exchanges and processes this information, customers, brokers and insurers would be helped,” says Zühr.

Automatic collaboration: The systems are connected

On one platform, customers could post their risks, brokers could offer suitable products and insurers could ultimately provide the appropriate cover. For my colleague Marc Philipp Gösswein, responsible for the insurance business in the mgm management, this scenario remains the big goal: “In the best case, the customer does not have to log in at all, because the customer systems are at least partially connected to any platform of the broker.”

What’s more, thanks to new technologies, companies could in future also digitally link production plants and process control systems, for example, and automatically monitor whether and when a risk becomes a hazard. “We are probably still five to ten years away from this,” estimates colleague Marc Philipp. “But that will come, because the preparation and elaboration of one’s own risk position with better measurability and a selective presentation of risks will ultimately have an impact on the sums insured and thus the premiums,” he is convinced.

Digitalization means platform – means give and take

The question of who could develop and operate such software or a platform is still open. As is well known, the industry is very sceptical about a solution in which market participants are among the operators. A dual role a la Amazon is therefore not supported in the insurance world. In addition, another solution seems necessary that offers interoperability and thus the possibility of switching to other providers or, alternatively, can be operated autonomously with changing constellations. In the automotive industry it has long been common practice to make joint investments in platforms, components and production chains. Large insurers have also been sharing certain data for many years, for example in the field of natural disasters or in the transport sector. There are already very well-used technical services for this purpose, which identify non-critical transport routes, for example. This data could also be seamlessly integrated on one platform.

In view of the potential players on the pitch, some players are thinking of changing tactics. Because when a software-driven company like Amazon or Google thinks of the insurance market, for example, value-added services and services come into focus. For example, there are certainly insurance customers who would like to use a platform to obtain information that they would otherwise not be able to obtain easily. This could be, for example, the coverage of comparable companies, similar size and country distribution, or which claims there have been in recent years and how they have been settled. Such services must be thought of early on.

Rejection of interface optimization

Couldn’t a mere interface optimization between the industry’s systems be enough to link quotation software, underwriting tools and inventory management systems? For Benjamin Zühr from GGW, this is not useful in the long run. “Then maybe the provider who has the most money wins the whole thing and not the one who ends up with the best product,” he is concerned. After all, it would be a heck of a job to connect all the individual platforms and individual products with each other via interfaces. “If you have many lines of business with a variety of insurance types in your portfolio and work with five or six insurers in each case, you will never get anywhere”.

This text was created in the context of a project cooperation between mgm and the insurance broker Gossler, Gobert & Wolters Gruppe (GGW) from Hamburg. In the series different participants write from and about the practice.

Bildquelle: tele52 / Shutterstock

Neueste Kommentare